Living Trusts

You have a will – so why would you want a Living Trust?

Contrary to what you’ve probably heard, a will may not be the best plan for you and your family, primarily because a will does not avoid probate when you die. A will must be verified by the probate court before it can be enforced.

Also, because a will can only go into effect after you die, it provides no protection if you because physically and mentally incapacitated. So the court could take control of your assets before you die – a concern of millions of older Americans and their families. Fortunately, there is a simple and proven alternative to a will – the revocable living trust. It avoids probate and lets you keep control of your assets while you are living even if you become incapacitated – and after you die.Probate is the legal process through which the court sees that, when you die, your debts are paid and your assets are distributed according to your will. If you don’t have a valid will, your assets are distributed according to state law.

WHAT’S SO BAD ABOUT PROBATE?

- It can be expensive! Legal/executor fees and other cost must be paid before your assets can be fully distributed to your heirs. If you own property in other states, your family could face multiple probates, each one according to the laws in the state. Because these costs can vary widely, be sure to get an estimate.

- It takes time, usually nine months to two years, but often longer. During part of this time, assets are usually frozen so an accurate inventory can b taken. Nothing can be distributed or sold without court and/or executor approval. If your family need money to live on, they must request a living allowance, which may be denied.

- Your family has no privacy. Probate is a public process, so any Interested party” can see what you owed and whom you owed. the process ‘invites’ disgruntled heirs to contest your will and can expose your family to unscrupulous solicitors.

- Your family has no control. The probate process determines how much it will cost, how long it will take, and what information is made public.

DOESN’T JOINT OWNERSHIP AVOID PROBATE?

Not really. Using joint ownership usually postpones probate. With does transfer to the surviving owner without probate. But if that owner dies without adding a new joint owner, or if both owners die at the same time, the asset must be probated before it can go to the heirs.

Watch out for other problems. When you add a co-owner, you lose control. Your chances of being named in a lawsuit and of losing the asset to a creditor are increased. There could be gift and/or income tax problems. And since a will does not control most jointly owned assets, you could disinherit your family.

With some assets, especially real estate, all owners must sign to sell or refinance. So if a co-owner becomes incapacitated, you could find yourself with a new “co-owner” – the court – even if the incapacitated owner is your spouse.

WHY WOULD THE COURT GET INVOLVED AT INCAPACITY?

If you cannot conduct business due to mental or physical incapacity (Alzheimer’s, stroke, heart attack, etc.), only a court appointee can sign for you – even if you have a will. (Remember a will only goes into effect after you die.)

Once the court gets involved, it usually stays involved until you recover or die. The court, not your family, controls how your assets are used to care for you. This public process can be expensive, embarrassing, time consuming and difficult to end if you recover. It does replace probate at death, so your family may have to go through probate court twice!

DOES A DURABLE POWER OF ATTORNEY PREVENT THIS?

A durable power of attorney lets you name someone to manage your financial affairs if you are unable to do so. However, many financial institutions will not honor one unless it is on their form. And, if accepted, it may work too well – giving someone a “blank check” to do whatever he/she wants with your assets. It can be very effective when used with a living trust, but risky when used alone.

WHAT IS A LIVING TRUST?

A living trust is a legal document that, just like a will, contains your instructions for what you want to happen to your assets when you die. But, unlike a will, a living trust avoids probate at death, can control all of your assets, and prevents the court from controlling your assets if you become incapacitated.

HOW DOES A LIVING TRUST AVOID PROBATE AND PREVENT COURT CONTROL OF ASSETS AT INCAPACITY?

When you set up a living trust, you transfer your assets from your name to the name of your trust, which you control – such as from “Bob and Sue Smith, husband and wife” to “Bob and Sue Smith trustees under trust dates (month/day/year).”

Legally you no longer own anything (don’t panic: everything now belongs to your trust), so there is nothing for the courts to control when you die or become incapacitated. The concept is very simple, but this is what keeps you and your family out of the courts.

DO I LOSE CONTROL OF THE ASSETS IN MY TRUST?

Absolutely not. You keep full control. As trustee of your trust, you can do anything you could do before – buy/sell assets, change or even cancel your trust (that’s why it’s called a revocable living trust). You even file the same tax returns. Nothing changes but the names on the titles.

IS IT HARD TO TRANSFER ASSETS INTO MY TRUST?

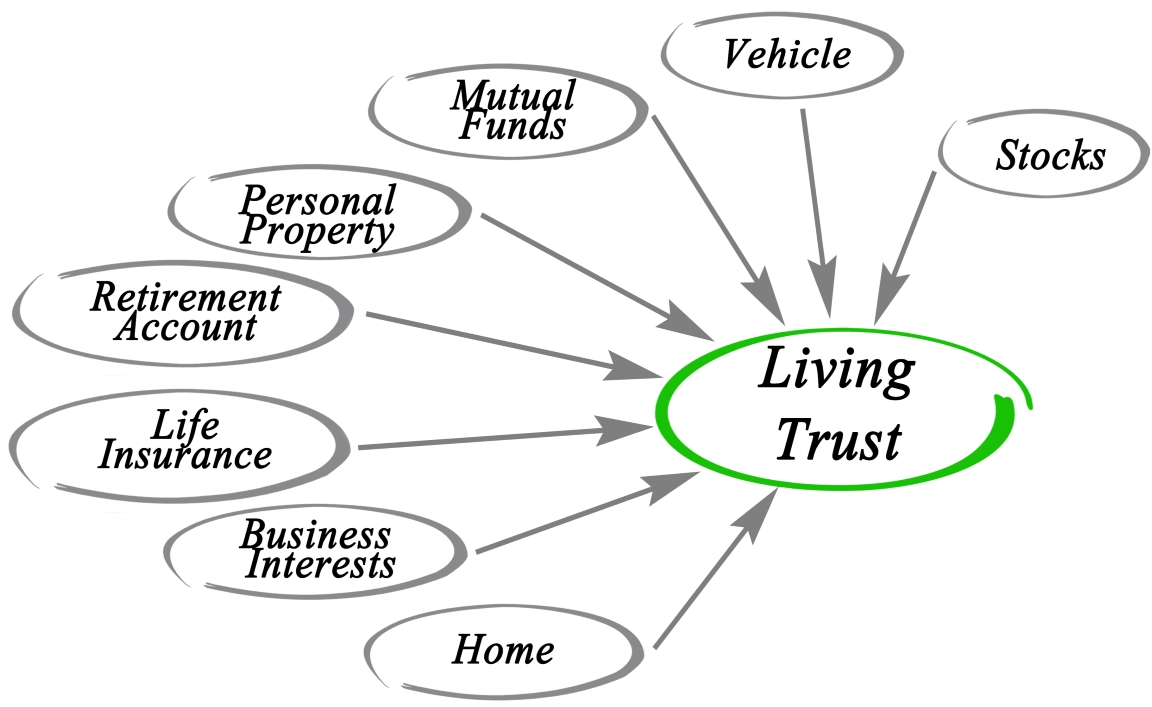

No, you and your attorney, trust officer, financial adviser and insurance agent can help. You need to change titles on real estate (in- and out-of-state) and other titled assets (stocks, CDs, bank accounts, other investments, insurance, etc.). Most living trusts include jewelry, clothes, art, furniture, and other assets that do not have titles.

Also, beneficiary designations on some assets (like insurance) should be changed to your trust so the court can’t control them if a beneficiary is incapacitated or no longer living when you die. (IRA, 401(k), etc. can be exceptions.)

DOES THIS TAKE A LOT OF TIME?

It will take some time – but you can do it now, or you can pay the courts and attorneys to do it for you later. One of the benefits of a living trust is that all of your assets are brought together under one plan. Don’t delay “funding” your trust. It can only protect assets that have been transferred into it.

SHOULD I CONSIDER A CORPORATE TRUSTEE?

You may decide to be the trustee of your trust. However, some people select a corporate trustee (bank or trust company) to act as trustee or co-trustee now, especially if they don’t have the time, ability or desire to manage their trusts, or if one or both spouses are ill. Corporate trustees are experienced investment manager, they are objective and reliable, and their fees are usually very reasonable.

IF SOMETHING HAPPENS TO ME, WHO HAS CONTROL?

If you and your spouse are co-trustees, either can act and have instant control if one becomes incapacitated or dies. If something happens to both of you, or if you are the only trustee, the successor trustee you personally selected will step in. If a corporate trustee is already your trustee or co-trustee, they will continue to manage your trust for you.

WHAT DOES A TRUSTEE OR SUCCESSOR DO?

If you become incapacitate, your successor trustee looks after your care and manages your financial affairs for as long as needed, using your assets to pay your expenses. If you recover, you automatically resume control. When you die, your successor trustee pays your debts and distributes your assets. All this is done quickly and privately, according to instructions in your trust, without court interference.

WHO CAN BE A SUCCESSOR TRUSTEE?

Successor trustees can be individuals (adult children, other relatives, or trusted friends) and/or a corporate trustee. If you choose an individual, you should name more than one in case your first choice is unable to act.

DOES MY TRUST END WHEN I DIE?

Unlike a will, a trust doesn’t have to die with you. Assets can stay in your trust, managed by the trustee you selected, until your beneficiaries reach the age(s) you want them to inherit. Your trust can continue longer to provide for a loved one with special needs, or to protect assets from beneficiaries’ creditors, ex-spouses and future death taxes.

DOES A TRUST IN A WILL DO THE SAME THING?

Not quite. A will can contain wording to create a testamentary trust to save estate taxes, care for minors, etc. But because it is part of your will, this trust cannot go into effect until after you die and the will is probated. So it does not avoid probate and provides no protection at incapacity.

IS A LIVING TRUST EXPENSIVE?

Not when compared to all the costs of court interference at incapacity and death. How much you pay will depend on how complicated your plan is.

HOW LONG DOES IT TAKE TO GET A LIVING TRUST?

It should only take a few weeks to prepare the legal documents after you make the basic decisions.

SHOULD I HAVE AN ATTORNEY DO MY TRUST?

Yes, but you need the right attorney. A local attorney who has considerable experience in living trusts will be able to give you valuable guidance and peace of mind that your trust is prepared properly. In some states, qualified paralegals can also prepare trust documents, but they cannot give you legal advice.

IF I HAVE A LIVING TRUST, DO I STILL NEED A WILL?

Yes, you need a “pour-over” will that acts as a safety net if you forget to transfer an asset to your trust. When you die, the will “catches” the forgotten asset and send it into your trust. The asset may have to go through probate first, but it can then be distributed as part of your living trust plan.

IS A LIVING WILL THE SAME AS A LIVING TRUST?

No. A living trust is for financial affairs. A living will is for medical affairs – it lets other know how you feel about life support in terminal situations.

ARE LIVING TRUSTS NEW?

No, they have been used successfully for hundreds of years.

WHO SHOULD HAVE A LIVING TRUST?

Age, marital status and wealth don’t really matter. If you own titled assets and want your loved ones (spouse, children, or parents) to avoid court interference at your death or incapacity, consider a living trust. You may also want to encourage other family members to have one so you won’t need to deal with the courts at their incapacity or death.

Read all about The Probate Process here.